Returning to work after a two-week holiday and it’s good to know that at least in the airline industry not much has happened! If only it were the same in other areas….

Airlines Return to Profitability as Capacity Carefully Managed

The good news is that many of the major airlines around the world have been reporting their second quarter results in the last week and for many carriers they are certainly a lot better than this time last year and for many the third quarter outlook is better than expected. Interestingly many airline CEOs dodged the corporate demand issue focussing on the strength of the leisure market whilst others admitted it was a slower recovery than they expected but in the round, we appear to finally be working in an industry looking forward rather than wondering what next. Let’s hope that nothing happens to dampen that recovery.

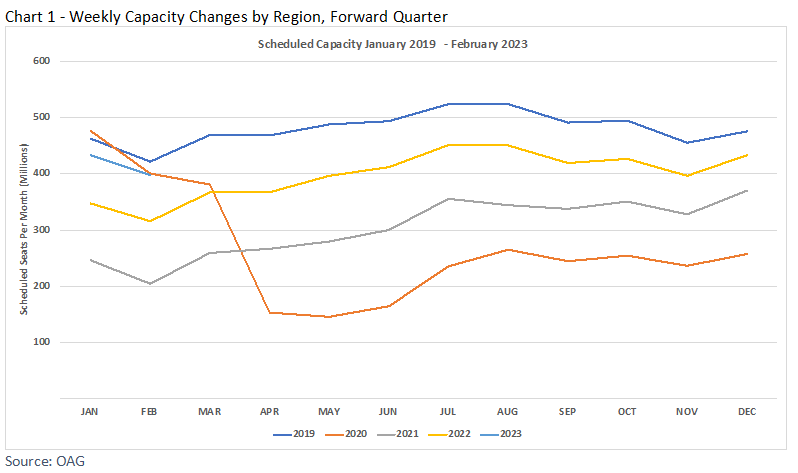

As is always the case the next few weeks before the US Thanksgiving period is a quiet time for capacity, the winter season has started, aircraft and crews are finally being rested and global capacity has settled at just below 90 million seats this week. In comparison to last year, this week will see 19% more capacity, but in comparison to the pre-pandemic level of 107 million scheduled seats in 2019, we are still some 16% adrift; with many airlines indicating that they will be operating less capacity this winter, bridging that capacity gap - certainly in the first half of 2023 - is looking increasingly unlikely.

Looking into the new year, January scheduled capacity currently stands at 433 million. With the usual ongoing capacity cuts we can expect that to settle at around 410 million, suggesting a 14% shortfall against the 2020 capacity point when, of course, Covid-19 was just a small news story for most of us.

North America's Recovery Fuelled by Strong Growth of LCCs (Low-Cost Carriers)

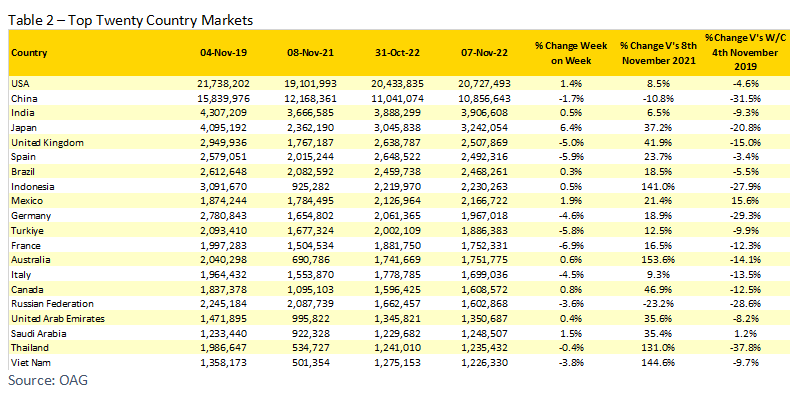

At the regional market level, we have noted before that some markets now offer more capacity than in 2019 with Central Asia an incredible 25% up, and having worked there recently it really is a rapidly growing market. However, the small size of those markets hardly moves the global needle of recovery.

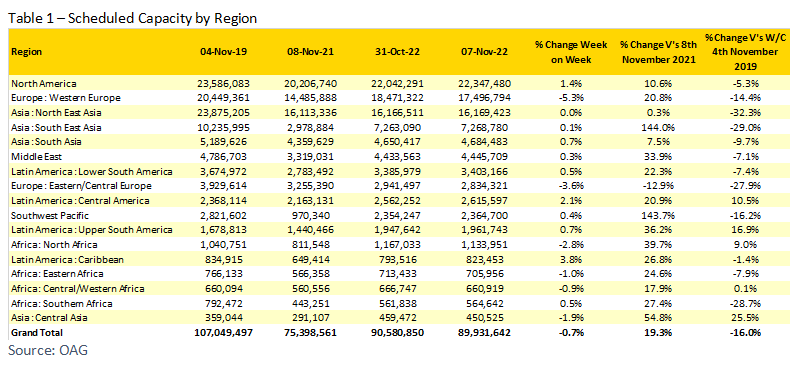

Positively North America (particularly the United States) is now within touching distance of a full recovery, fuelled by the strong growth of the low-cost sectors; carriers like Frontier have boldly entered legacy-dominated markets, such as Dallas Ft Worth, as they bravely open new frontiers of revenue.

Most regional markets report minimal capacity change week-on-week and where there is any change the capacity reductions are all explainable and expected. Western Europe has the largest reduction in capacity with the loss of a million seats week-on-week but it’s nothing to panic about, much of that capacity was bringing back returning half-term holiday makers and is part of the typical programme that we see each year. Those changes aside there are only minimal changes in capacity around the globe which in turn leads to the 0.7% change in capacity week on week; this time last year we saw a 3.1% week-on-week reduction in capacity with a 10.6% change in North East Asia alone…things are so much better now!

Throughout our weekly updates through the pandemic, we have noted that the “devil is in the detail” and that the more granular the data analysis then the more insights that are possible and this week is no different.

North East Asian capacity (at a regional level) is unchanged week-on-week, but that disguises another series of lockdowns in China and a further nudging down of capacity. Whilst Japan reports one of its strongest increases for some months with a 6.4% week-on-week increase. However, Japan's dependency on Chinese connectivity is hampering a complete recovery, and capacity remains 20% below 2019 levels.